Islamic Forex accounts, also known as swap-free accounts, are designed to comply with Shariah principles by eliminating overnight interest (riba) on open positions. These accounts allow Muslim traders to participate in global financial markets without incurring or receiving swap charges on leveraged trades.

Below is a review of the best Forex brokers offering Islamic accounts based on regulation, trading costs, platform availability, leverage structure, asset diversity, and overall account transparency

| vt markets | |||

| fxcm | |||

| LiteFinance | |||

| 4 |  | OX Securities | ||

| 5 |  | GrandCapital | ||

| 6 |  | instaforex | ||

| 7 |  | NAGA | ||

| 8 |  | orbex | ||

| 9 |  | xChief | ||

| 10 |  | HEADWAY |

Trustpilot Rankings of Islamic Account (Swap-Free) Forex Brokers

Trustpilot ratings offer valuable insight into real user experiences with brokers that provide Islamic (swap-free) accounts. While regulation confirms legal oversight, Trustpilot reflects trader satisfaction in areas such as withdrawal reliability, spread transparency, customer support responsiveness, execution speed, and compliance with Shariah-based swap-free policies.

Broker Name | Trustpilot Rating | Number of Reviews |

856 | ||

OX Securities | 715 | |

2,462 | ||

Orbex | 115 | |

4,257 | ||

LiteFinance | 531 | |

Headway | 990 | |

xChief | 62 | |

Grand Capital | 87 | |

InstaForex | 469 |

Islamic Accounts Brokers with the Lowest Spread Conditions

When selecting an Islamic (swap-free) forex broker, spreads become even more important because overnight swap charges are removed. Since brokers cannot charge interest, some may apply wider spreads or administrative fees instead.

Broker Name | Min. Spread |

0.0 Pips | |

KOT4X | 0.0 Pips |

Lirunex | 0.0 Pips |

Scope Markets | 0.0 Pips |

0.0 Pips | |

0.0 Pips | |

InstaForex | 0.0 Pips |

FXCM | 0.2 Pips |

NAGA | 0.2 Pips |

Grand Capital | 0.4 Pips |

Account Type Options Offered by Swap-Free Brokers

Forex brokers that provide Islamic (swap-free) accounts usually integrate this feature into multiple account structures rather than offering a single standalone account. The goal is to accommodate different trading styles, capital sizes, and execution preferences while maintaining Shariah compliance by removing overnight interest charges.

Broker Name | Account Types | Max. Leverage |

VT Markets | Standard STP, RAW ECN, Cent STP, Cent ECN, Demo | 1:500 |

FXCM | CFD account, Active Trader account, Corporate account | 1:1000 |

LiteFinance | CLASSIC, ECN | 1:1000 |

OX Securities | Standard, Pro, Swap Free, Demo | 1:500 |

Standard, MT5, Micro, ECN Prime, Swap Free | 1:1000 | |

Insta.Standard, Insta.Eurica, Cent.Standard, and Cent Eurica | 1:1000 | |

Trive Invest | Classic, Classic Gold, Premium, Swap Free, Demo | 1:1000 |

Markets.com | Retail, Professional | 1:300 |

ForexMart | Classic, Cent, Pro, Zero Spread | 1:3000 |

Taurex | Standard Zero, Pro Zero, Raw | 1:2000 |

Available Assets and Instruments in Islamic Accounts Brokers

Islamic (swap-free) Forex brokers typically provide access to a wide range of tradable instruments while removing overnight interest charges. However, the availability of assets under swap-free conditions may vary depending on the broker’s internal policy, Shariah compliance framework, and risk model.

Broker Name | Number of Instruments |

FXCM | 13,000+ |

OX Securities | 10,000+ |

Exclusive Markets | 5000+ |

VT Markets | 1,000+ |

LiteFinance | 600+ |

Fxview | 500+ |

400+ | |

Windsor Brokers | 190+ |

150+ | |

AdroFX | 115+ |

Top 7 Forex Brokers with Islamic Accounts (Swap-Free)

Below are seven well-known Forex brokers that provide Islamic (swap-free) accounts, allowing traders to operate in compliance with Sharia principles while maintaining competitive trading conditions.

VT Markets

VT Markets is a multi-asset Forex and CFD broker headquartered in Australia, offering access to more than 1,000 tradable instruments across seven financial markets. The broker facilitates over 30 million trades per month and serves more than 400,000 active traders globally.

It operates under multiple regulatory entities, including ASIC in Australia, FSCA in South Africa, and FSC in Mauritius. While ASIC is considered Tier-1, the ASIC entity mainly serves wholesale clients, whereas global retail traders are typically onboarded under offshore or Tier-2 jurisdictions.

VT Markets dashboard provides four primary live account types: Standard STP, RAW ECN, Cent STP, and Cent ECN. The minimum deposit starts from $50, with leverage reaching up to 1:500 depending on the entity. Spreads begin from 0.0 pips on ECN accounts, while STP accounts offer commission-free trading with slightly wider spreads.

Trading is supported via MetaTrader 4, MetaTrader 5, WebTrader+, and the proprietary VT Markets mobile app. The broker also offers copy trading and PAMM solutions, Islamic accounts, promotional bonuses, and VPS reimbursements.

Although VT Markets verification promotes strong trading infrastructure, concerns remain regarding offshore onboarding transparency and mixed third-party review scores.

Account Types | Standard STP, RAW ECN, Cent STP, Cent ECN, Demo |

Regulating Authorities | ASIC (516246), FSCA (50865), FSC Mauritius (GB23202269) |

Minimum Deposit | $50 |

Deposit Methods | Credit/Debit Cards, Bank Wire, Neteller, Skrill, UnionPay, Fasapay |

Withdrawal Methods | Credit/Debit Cards, Bank Wire, Neteller, Skrill, UnionPay, Fasapay |

Maximum Leverage | Up to 1:500 (entity dependent) |

Trading Platforms & Apps | MetaTrader 4, MetaTrader 5, WebTrader+, VT Markets Mobile App |

VT Markets Pros and Cons

VT Markets offers a competitive trading environment supported by solid infrastructure and diverse market access. However, certain limitations in fees, platform features, or regional restrictions may affect specific traders. Below is a balanced overview of its strengths and weaknesses.

Pros | Cons |

Multi-jurisdiction regulation (ASIC, FSCA, FSC) | ASIC entity limited to wholesale clients |

Spreads from 0.0 pips on ECN accounts | Mixed third-party trust scores |

Low minimum deposit from $50 | No excess loss insurance |

1:500 leverage for eligible clients | Withdrawal fees may apply |

MT4, MT5, WebTrader+, and mobile app | Crypto offering relatively limited |

Copy trading and PAMM available | Not available in several restricted countries |

Islamic account option | Transparency concerns after Vantage separation |

FXCM

FXCM, short for Forex Capital Markets, is a long standing Forex and CFD broker founded in 1999 with a multi regulated structure across several jurisdictions. The broker holds licenses from FCA, ASIC, CySEC, ISA, and FSCA, which supports a broad international presence and adds credibility through Tier 1 oversight in key regions.

FXCM’s history includes major regulatory setbacks, including a 2017 CFTC enforcement action and a subsequent exit from the US market. After FXCM Group filed for bankruptcy in 2017, Jefferies Financial Group acquired the company, and FXCM continued operating under non US entities.

After completing the FXCM registration, the broker offers access to multiple markets such as Forex, indices, commodities, crypto CFDs, and shares. Pricing is positioned as competitive with spreads from 0.2 pips and generally no trading commissions on CFDs, depending on the product and entity.

Accounts are structured around CFD, Active Trader, and Corporate options, with Active Trader designed for high volume clients. Platform support includes MT4, TradingView integration, and TradeStation, plus proprietary tooling like Trading Station and automation through Capitalise AI.

Key non trading considerations include an inactivity fee and bank wire withdrawal fees, which can impact long term cost efficiency.

Account Types | CFD account, Active Trader account, Corporate account |

Regulating Authorities | FCA, CySEC (392/20), ASIC, FSCA (46534), ISA |

Minimum Deposit | $50 |

Deposit Methods | Visa, MasterCard, Bank Wire Transfer, Neteller, Skrill |

Withdrawal Methods | Visa, MasterCard, Bank Wire Transfer, Neteller, Skrill |

Maximum Leverage | Up to 1:1000, entity dependent |

Trading Platforms and Apps | MT4, TradingView, TradeStation, Trading Station |

FXCM Pros and Cons

The broker stands out for its structured pricing model and features like FXCM rebate. At the same time, some operational constraints and policy conditions should be carefully considered before opening an account.

Pros | Cons |

Multi regulated structure across FCA, ASIC, CySEC, ISA, FSCA | 2017 CFTC case and US exit remain a reputational risk |

Segregated accounts under FCA and ASIC rules | Bankruptcy history tied to FXCM Group in 2017 |

Negative balance protection across regulated entities | Inactivity fee applies after long dormancy |

Investor compensation available under FCA and CySEC regimes | Bank wire withdrawals can carry a $40 fee |

Spreads from 0.2 pips with no commission on many CFD products | Leverage varies heavily by entity and region |

Strong platform coverage via MT4, TradingView, TradeStation | Certain countries restricted, including USA |

Active Trader benefits for high volume clients | Some past regulatory actions beyond CFTC |

LiteFinance

LiteFinance is a long established Forex and CFD broker active since 07/2005, offering access to Currency pairs, stocks, indices, and metals. The broker promotes high leverage up to 1:1000 under its global entity and supports CLASSIC and ECN accounts, including swap free versions, that are choosable after LiteFinance verification.

Regulation depends on the branch you choose. EU clients trade under LiteForex Europe Ltd with CySEC Tier 1 oversight, ICF coverage up to €20,000, segregated funds, and negative balance protection, but leverage is limited to 1:30.

Global clients usually trade under the Mauritius FSC entity, where leverage can reach 1:1000, but investor compensation is not listed and segregated funds are shown as not provided in the table.

Pricing differs by account type (available to see in LiteFinance dashboard). CLASSIC trading runs with spreads from 1.8 points and no commission, while ECN offers spreads from 0.0 points with commissions that can reach $5 per lot on FX majors.

Non trading costs include a $10 inactivity fee after 3 months of no trading, plus standard swap mechanics and possible conversion charges.

The broker supports MT4, MT5, cTrader, and a mobile app, and it also offers LiteFinance copy trading, PAMM, promotions, and trading contests. Trust scores are mixed across platforms, so entity selection and fee checks matter before funding.

Account Types | CLASSIC, ECN, Swap Free versions, Demo |

Regulating Authorities | CySEC (EU entity), FSC Mauritius (global entity) |

Minimum Deposit | $50 |

Deposit Methods | Credit and Debit Cards, Bank Wire, STICPAY, Perfect Money, Africa Mobile Money, Volet |

Withdrawal Methods | Credit and Debit Cards, Bank Wire, STICPAY, Perfect Money, Africa Mobile Money, Volet |

Maximum Leverage | Up to 1:1000 (1:30 under CySEC branch) |

Trading Platforms and Apps | MT4, MT5, cTrader, Mobile App |

LiteFinance Pros and Cons

LiteFinance provides traders with multiple account options and competitive spreads. Despite these advantages, there may be areas such as withdrawal policies or platform flexibility that require attention.

Pros | Cons |

Long operating history since 2005 | Investor protection varies sharply by entity |

ECN account with spreads from 0.0 points | FSC entity table shows no segregated funds |

High leverage up to 1:1000 for global clients | $10 inactivity fee after 3 months |

MT4, MT5, cTrader, and mobile app supported | Limited account type variety, mainly CLASSIC and ECN |

Copy trading and PAMM available | No 24/7 customer support |

Swap free options available | ECN commissions apply, including $5 per lot on FX majors |

Multiple funding options including local methods | Restricted regions include US and EU under global branch |

OX Securities

OX Securities is a Forex and CFD broker operating since 2013 under the legal name Ox Securities Ltd, registered in St. Vincent and the Grenadines with number 25509 BC 2019. The broker provides access to 10,000+ CFDs and promotes zero minimum deposit, market execution, and leverage up to 1:500.

Account choice after OX Securities registration is simple and includes Standard, Pro, and Swap Free, plus a demo mode for testing. Trading conditions stay consistent across accounts in core settings, including 0.01 minimum order size, margin call at 90%, and stop out at 20%, while pricing changes by spread and commission.

Standard and Swap Free start from 1 pip with $0 commission, while Pro targets spreads from 0 pips with a $7 per round lot fee.

The listed regulator is SVGFSA, which is not considered a top tier authority, so broker level protections matter.

OX Securities states segregated funds, negative balance protection, and coverage up to €20,000 under the Financial Commission. Funding options depends on OX Securities verification and supports bank transfers, cards, crypto, and e-payment systems such as Skrill and Neteller, with many deposit methods shown as fee free and fast.

Platforms appear inconsistent across sections, with IRESS highlighted as the main terminal while account tables reference MT4 and MT5. Trust signals are mixed across review sites, so traders should verify platform access, entity terms, and withdrawal conditions before funding.

Account Types | Standard, Pro, Swap Free, Demo |

Regulating Authorities | SVGFSA |

Minimum Deposit | $0 |

Deposit Methods | Bank Transfers, Crypto, E Payment Systems, Credit and Debit Cards |

Withdrawal Methods | Bank Transfers, Crypto, E Payment Systems, Credit and Debit Cards |

Maximum Leverage | 1:500 |

Trading Platforms & Apps | IRESS (account table also references MT4 and MT5) |

OX Securities Pros and Cons

OX Securities combines cost efficiency with regulatory transparency, making it attractive to many traders. Nevertheless, certain product limitations or service conditions may not suit all trading styles.

Pros | Cons |

10,000+ CFDs across multiple markets | Regulation is SVGFSA, not top tier |

$0 minimum deposit advertised | Platform information is inconsistent across sections |

Leverage up to 1:500 | Live chat access may be bot only based on testing |

Swap free account available | Trust scores vary widely across review sources |

Pro account spreads from 0 pips available | Crypto leverage details are not clearly specified |

Segregated funds and negative balance protection stated | Swap rates are not disclosed on the website |

PAMM investment option offered | 24/7 support is not available |

Grand Capital

Grand Capital is an offshore brokerage established in 2006 and registered in Seychelles. Over more than 16 years of operation, the company has expanded its services to over 140 countries and reports serving more than 1.5 million clients worldwide.

The broker does not operate under a major tier-1 regulator. However, it is a member of The Financial Commission, which provides an external dispute resolution mechanism and a compensation fund of up to €20,000 per client. Despite this, it does not offer formal negative balance protection under a top-tier regulatory framework.

Grand Capital provides trading leverage up to 1:1000 and allows traders to start with a minimum deposit as low as $10 on its Micro account. The broker offers access to more than 500 tradable instruments across Forex, Stocks, ETFs, Cryptocurrencies, Indices, Metals, Commodities, Energy products, and Bonds.

Clients can choose between multiple account types, including Standard, MT5, Micro, ECN Prime, and Swap Free account. Trading is supported via MetaTrader 4, MetaTrader 5, and WebTrader platforms. Additional services such as copy trading, investment portfolios, bonuses, and trading competitions are also available.

However, traders should carefully evaluate risk factors, especially considering the broker’s offshore structure and mixed public trust ratings.

Account Types | Standard, MT5, Micro, ECN Prime, Swap Free |

Regulating Authorities | Member of The Financial Commission |

Minimum Deposit | $10 |

Deposit Methods | Bank Cards, Bank Transfer, E-payments, Crypto, Local Exchange |

Withdrawal Methods | Bank Cards, Bank Transfer, E-payments, Crypto, Local Exchange |

Maximum Leverage | 1:1000 |

Trading Platforms & Apps | MetaTrader 4, MetaTrader 5, WebTrader |

Grand Capital Pros and Cons

Grand Capital delivers a diversified trading experience with access to various financial instruments. While its core features are strong, potential drawbacks in execution structure or fee layers should be reviewed.

Pros | Cons |

500+ tradable instruments across multiple markets | No tier-1 regulatory license |

Leverage up to 1:1000 | No formal negative balance protection |

$10 minimum deposit available | $500 minimum for ECN Prime account |

Copy trading and investment portfolios | $15 inactivity fee after 90 days |

Deposit bonuses and trading contests | Mixed user trust reviews |

24/7 multilingual customer support | Limited platform diversity |

InstaForex

InstaForex is a multi-asset Forex and CFD broker founded in 2007 and headquartered in St. Vincent and the Grenadines. The company operates under a BVI FSC license and claims to serve over 7 million clients globally.

The broker offers access to 5 major markets, including Forex, stocks, indices, commodities, cryptocurrencies, and futures CFDs. When completing InstaForex registration, traders can choose between four main account types: Insta.Standard, Insta.Eurica, Cent.Standard, and Cent.Eurica, with a minimum deposit starting from just $1.

Maximum leverage reaches 1:1000, making it attractive for high-risk traders. Platforms include MetaTrader 4, MetaTrader 5, WebTrader, MultiTerminal, and a proprietary mobile app. Instant and market execution models are supported.

Spreads start from 0 on Eurica accounts, while Standard accounts apply variable spreads. However, InstaForex does not provide segregated funds, negative balance protection, or investor compensation under its offshore entity.

Trust scores remain mixed, with a 2.5/5 rating on Trustpilot and 1.3/5 on ForexPeaceArmy. While the broker offers bonuses, copy trading, PAMM accounts, and 24/7 multilingual support, regulatory strength and fee transparency remain key considerations before opening an account.

Account Types | Insta.Standard, Insta.Eurica, Cent.Standard, Cent.Eurica, Demo |

Regulating Authorities | BVI FSC (Tier 3) |

Minimum Deposit | $1 |

Deposit Methods | Bank Transfer, Skrill, Neteller, WebMoney, PayCo, Crypto (BTC, LTC, ETH, USDT), Visa/MasterCard |

Withdrawal Methods | Bank Transfer, Skrill, Neteller, WebMoney, PayCo, Crypto, Visa/MasterCard |

Maximum Leverage | Up to 1:1000 |

Trading Platforms & Apps | MetaTrader 4, MetaTrader 5, WebTrader, Mobile App, MultiTerminal |

InstaForex Pros and Cons

InstaForex maintains a balanced framework between pricing, regulation, and product range. Still, like any broker, it presents both advantages and limitations that traders should evaluate carefully.

Pros | Cons |

Very low minimum deposit ($1) | No Tier-1 regulation |

High leverage up to 1:1000 | No segregated funds (offshore entity) |

4 account types including Cent accounts | No negative balance protection |

MT4 & MT5 support | Mixed trust scores |

Copy trading & PAMM available | Withdrawal fees apply |

24/7 multilingual support | Inactivity fee (€5 monthly after 3 months) |

NAGA

NAGA is a Germany-founded fintech brokerage established in 2015 and publicly listed on the Frankfurt Stock Exchange. The company operates through a multi-entity structure, serving European clients under CySEC (License 204/13) and international traders via its offshore arm.

Under the CySEC entity, clients benefit from segregated funds, negative balance protection, and Investor Compensation Fund coverage up to €20,000.

NAGA dashboard positions itself as a social-first trading ecosystem. With more than 1.5 million registered users globally, NAGA combines CFD trading, real stocks, crypto exposure, and NAGA copy trading under one unified platform. Its proprietary NAGA App integrates social feeds, trade sharing, and Autocopy functionality, allowing users to replicate strategies from top-performing traders.

NAGA offers six account tiers ranging from Iron to Crystal. The minimum deposit in all NAGA deposit and withdrawal methods starts at $250, while leverage is capped at 1:30 under EU regulation. Spreads begin from 0.2 pips on major FX pairs, with stock CFD commissions starting at €2.50 per trade. The broker also applies inactivity fees after 60 days.

With access to over 4,000 instruments across Forex, indices, stocks, ETFs, commodities, and crypto CFDs, NAGA targets both retail traders and social investors seeking a diversified, community-driven trading experience.

Account Types | Iron, Bronze, Silver, Gold, Diamond, Crystal, Demo |

Regulating Authorities | CySEC (204/13), Offshore Entity (Seychelles) |

Minimum Deposit | $250 |

Deposit Methods | Credit/Debit Cards, Bank Wire, Skrill, Neteller, Crypto (varies by region) |

Withdrawal Methods | Credit/Debit Cards, Bank Wire, Skrill, Neteller |

Maximum Leverage | 1:30 (EU Retail Clients) |

Trading Platforms & Apps | MetaTrader 4, MetaTrader 5, NAGA Web Platform, NAGA Mobile App |

NAGA Pros and Cons

NAGA appeals to traders seeking competitive spreads and structured account types. However, differences in leverage availability or asset depth may impact specific strategies.

Pros | Cons |

Regulated by CySEC (EU protection) | Leverage limited to 1:30 (EU rules) |

Investor Compensation Fund up to €20,000 | $50 inactivity fee after 60 days |

Strong social & copy trading ecosystem | Higher tiers require large deposits |

4,000+ tradable instruments | Spreads not the tightest in industry |

MT4, MT5 & Proprietary App | Offshore entity has lower protection |

4.5/5 Trustpilot rating | Withdrawal fees may apply depending on method |

What is Islamic (Swap-Free) Account?

An Islamic account, also known as a swap-free account, is a trading account designed to comply with Shariah law, which prohibits earning or paying interest (Riba). In standard Forex trading, positions held overnight incur swap or rollover interest based on interbank rates. Islamic accounts remove this interest component.

Instead of swap charges, brokers apply alternative cost structures that align with Islamic finance principles. These may include fixed administrative fees, wider spreads, or commission markups. The key objective is to ensure that no interest is charged or paid on overnight positions.

Islamic accounts are commonly available for Forex and CFD trading, including indices, commodities, and sometimes crypto CFDs. However, eligibility requirements may apply, and brokers often request proof of faith or additional verification to activate swap-free status.

These accounts are primarily intended for Muslim traders who wish to participate in financial markets without violating religious guidelines. However, many brokers structure them carefully to maintain commercial viability while adhering to compliance and risk management standards.

Pros and Cons of Islamic Accounts

Islamic accounts can be highly useful for position traders, but understanding alternative fee structures is essential before opening one. Table below is a full guide on its pros and cons.

Pros | Cons |

No overnight interest charges on open positions | Often includes negative balance protection |

Suitable for long-term holding strategies | Administrative or fixed holding fees may apply |

Shariah-compliant trading structure | Time limits on swap-free status (e.g., 5–14 days) |

Available across multiple asset classes | Not available on all instruments |

Often includes negative balance protection | Possible additional eligibility checks |

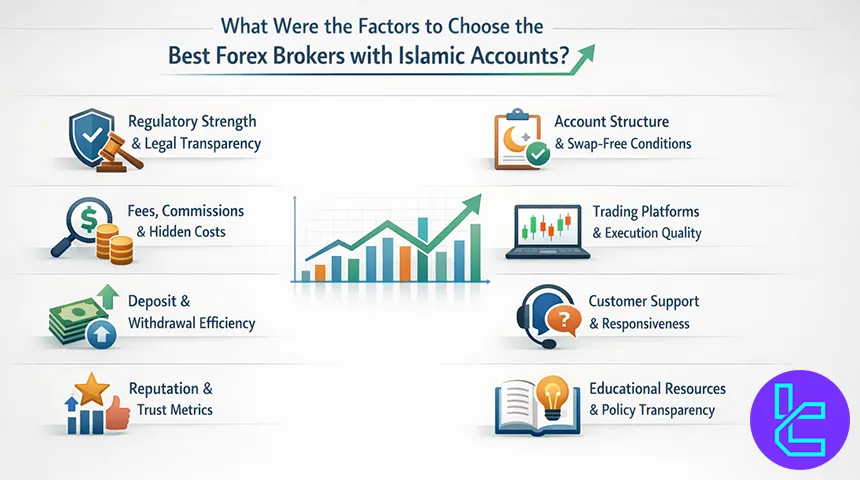

What Were the Factors to Choose the Best Forex Brokers with Islamic Accounts?

Choosing the best Forex brokers with Islamic (swap-free) accounts requires more than simply checking whether overnight swaps are removed. Since traders entrust real capital to these platforms, a structured and data-driven evaluation process is essential.

TradingFinder applies a comprehensive methodology built on 19 core data metrics to ensure transparency, objectivity, and practical relevance.

When reviewing brokers that offer Islamic accounts, the following factors receive special attention:

- Regulatory Strength and Legal Transparency: We verify licenses, supervising authorities, and investor protection frameworks to ensure client fund safety, compliance standards, and operational legitimacy;

- Account Structure and Swap-Free Conditions: We analyze how swap-free accounts are structured, whether administrative fees apply after a holding period, and if trading conditions differ from standard accounts;

- Fees, Commissions, and Hidden Costs: A detailed breakdown of spreads, commissions, inactivity charges, and alternative overnight costs helps determine the real long-term expense of a swap-free account;

- Trading Platforms and Execution Quality: We assess platform availability such as MT4, MT5, cTrader, and mobile apps, along with execution speed, liquidity access, and slippage control;

- Deposit and Withdrawal Efficiency: Funding methods, transaction processing times, and fee transparency are reviewed to evaluate capital accessibility and operational reliability;

- Customer Support and Responsiveness: Since Islamic accounts often require eligibility verification, we test support quality, multilingual availability, and dispute handling responsiveness;

- Reputation and Trust Metrics: Trustpilot scores, regulatory warnings, scam reports, and broker response behavior are incorporated into the overall credibility assessment;

- Educational Resources and Policy Transparency: We examine whether brokers clearly explain swap-free policies, Sharia compliance terms, and cost structures to prevent misunderstandings.

By integrating these structured metrics, TradingFinder identifies Forex brokers that not only offer Islamic accounts, but also deliver transparent pricing, reliable infrastructure, and regulatory security.

How Does Islamic Accounts Work?

Islamic accounts function similarly to standard trading accounts, with one key structural difference: overnight interest is removed.

Here is how the structure typically works:

- Position Opened: The trader opens a Forex or CFD trade normally;

- No Swap Applied: When the position remains open overnight, no rollover interest is charged or credited;

- Alternative Cost Model: Instead of swap, the broker may apply fixed daily administrative fee, wider spread pricing and flat commission per lot;

- Holding Period Limits: Some brokers allow swap-free conditions only for a limited number of days.

Execution, leverage, margin call, and stop-out rules usually remain identical to standard accounts. The main operational difference lies in overnight cost treatment.

Are Islamic Accounts Profitable for Brokers?

Islamic accounts remove overnight swap interest, but that does not mean brokers lose profitability. Instead of earning from rollover differentials between interest rates, brokers restructure their pricing models to maintain revenue neutrality.

In standard accounts, swap is derived from the interest rate differential between two currencies, plus a broker markup. In swap-free accounts, this revenue stream is replaced with alternative mechanisms such as:

- Fixed administrative fees applied after a holding period

- Slightly wider spreads across selected instruments

- Commission-based ECN pricing models

- Volume-driven revenue from higher trading activity

From a commercial perspective, brokers design Islamic accounts to remain economically balanced. If swap were completely removed without compensation, it would create arbitrage opportunities where traders exploit interest rate differentials risk-free. To prevent this, brokers introduce fair-use policies and time limits.

Ultimately, Islamic accounts can be just as profitable for brokers as standard accounts, provided pricing structures are adjusted transparently and sustainably.

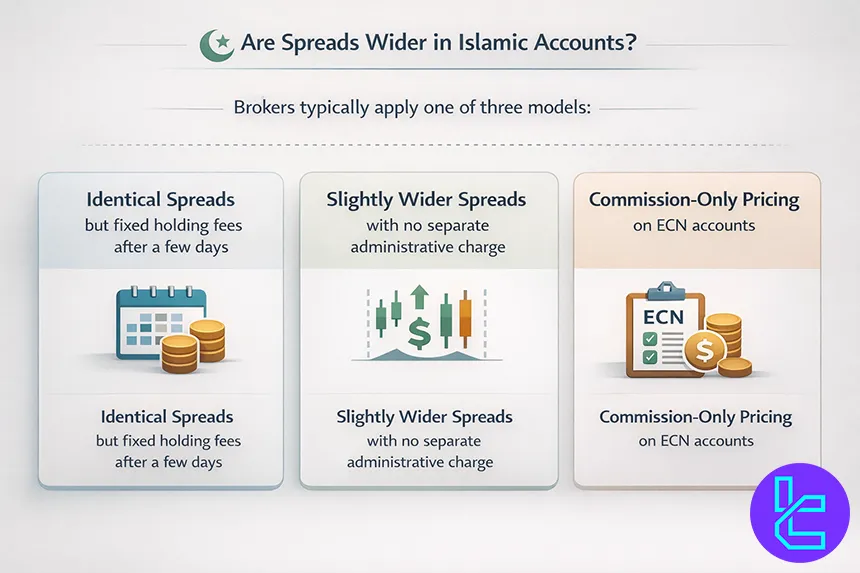

Are Spreads Wider in Islamic Accounts?

Spreads in Islamic accounts may be wider, but this depends entirely on the broker’s pricing policy. There is no universal rule requiring higher spreads.

Brokers typically apply one of three models:

- Identical spreads, but fixed holding fees after a few days

- Slightly wider spreads with no separate administrative charge

- Commission-only pricing on ECN accounts

For example, a standard account might offer EURUSD from 0.3 pips plus swap, while the Islamic version may offer 0.5 pips with no swap. The difference compensates for the removal of rollover revenue.

However, some regulated brokers maintain identical spreads between account types and instead enforce time-based swap-free limits, often between 5 and 14 days. After that period, administrative costs may apply.

The key factor is transparency. Traders should compare live spreads under real market conditions rather than relying solely on advertised minimums.

Do Commissions and Hidden Fees Increase in Swap-Free Accounts?

In many cases, commissions do not increase directly, but total trading costs may shift structurally. Islamic accounts often replace overnight interest with clearly defined administrative or service charges.

Common alternative cost structures include:

- Fixed daily fee per lot after a grace period

- One-time flat charge per trade

- Increased spread markups

- Volume-based minimum requirements

- Time restrictions on holding trades

Hidden fees are more likely when brokers fail to clearly document swap-free conditions. Reputable brokers disclose:

- The maximum number of swap-free days

- Administrative fee schedules

- Instruments excluded from swap-free status

- Conditions that may void Islamic eligibility

Before activating a swap-free account, traders should carefully review the broker’s Client Agreement and Contract Specifications.

A properly structured Islamic account should not contain “hidden” fees, but it may contain alternative cost mechanisms designed to offset the removal of swap.

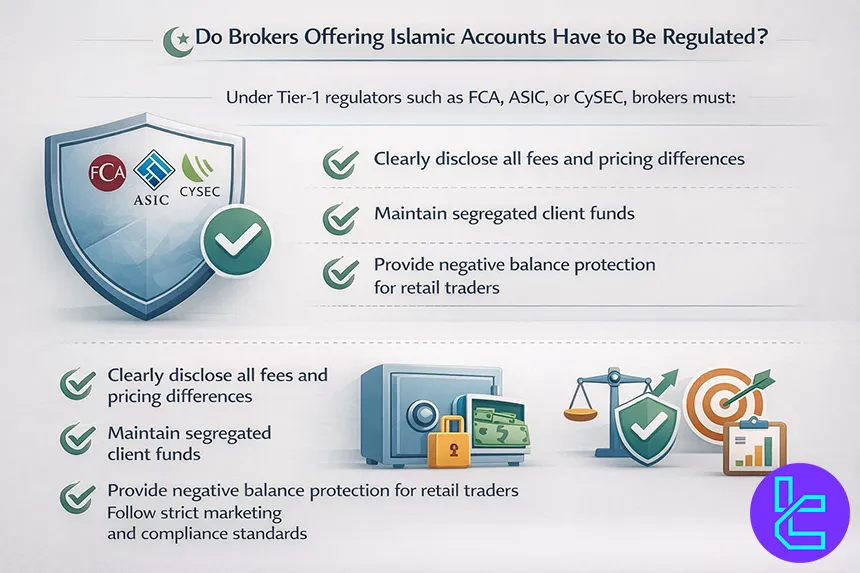

Do Brokers Offering Islamic Accounts Have to Be Regulated?

There is no global legal requirement forcing brokers to be regulated in order to offer Islamic accounts. However, regulation significantly improves client protection and fee transparency.

Under Tier-1 regulators such as FCA, ASIC, or CySEC, brokers must:

- Clearly disclose all fees and pricing differences

- Maintain segregated client funds

- Provide negative balance protection for retail traders

- Follow strict marketing and compliance standards

In contrast, offshore or lightly regulated brokers may offer swap-free accounts without strict oversight. While this does not automatically mean the broker is unsafe, the level of enforcement and dispute resolution mechanisms may be weaker.

Traders using Islamic accounts should prioritize brokers with strong regulatory backing, as this ensures transparent pricing and structured consumer protection.

Key Notes to Consider When Using Islamic Accounts Brokers

Before selecting a swap-free broker, traders should evaluate multiple strategic and regulatory factors. Islamic accounts are not automatically cheaper or safer than standard accounts; they simply follow a different cost structure.

Cost Structure Analysis

Before opening an Islamic account, traders should carefully evaluate the full pricing structure rather than focusing only on the absence of swap fees. A proper comparison helps identify whether the swap-free model is genuinely cost-efficient.

- Compare spreads between standard and Islamic accounts

- Confirm whether administrative fees apply after a holding period

- Check if specific instruments are excluded from swap-free conditions

Regulatory & Protection Factors

Regulatory oversight plays a major role in ensuring that swap-free conditions are applied transparently and fairly. Traders should verify that the broker operates under a recognized authority and follows structured compliance standards.

- Verify regulatory license and jurisdiction

- Confirm negative balance protection policy

- Review investor compensation coverage

Strategy Compatibility

Islamic accounts are not universally suitable for every trading style. The effectiveness of a swap-free model depends heavily on holding duration, trade frequency, and asset class selection.

- Long-term traders benefit most from swap-free conditions

- Scalpers should compare spread differences carefully

- Crypto CFD policies may differ from Forex instruments

Operational Conditions

Some brokers impose internal policies on swap-free accounts to prevent misuse or arbitrage exploitation. Understanding these operational terms is essential before activating the account.

- Some brokers limit swap-free status to verified Muslim clients

- Fair-use policies may restrict excessive long-term arbitrage strategies

- Demo testing is recommended before switching account types

Swap-Free Account Vs Other Account Types

When comparing a Swap-Free (Islamic) account with Standard and ECN accounts, the core trading mechanics remain largely similar. The primary difference lies in how overnight financing is handled.

While Standard and ECN accounts apply swap (rollover) interest on positions held overnight, Islamic accounts remove interest-based charges and often replace them with fixed administrative fees after a defined holding period.

Execution models, spreads, and liquidity access depend more on the broker’s infrastructure than the swap-free label itself. In many cases, Islamic accounts mirror either Standard or ECN structures, but with modified cost components to comply with Sharia principles.

Parameter | Islamic (Swap-Free) Account | Standard | ECN |

Order Routing | Usually STP or ECN, depending on broker structure | Mostly STP / Market Maker | Direct ECN / Raw liquidity providers |

Spread Type | Fixed or floating (similar to linked account type) | Mostly floating | Raw spreads from 0.0 pips |

Commission | Often none, but may include admin fee after X days | Usually $0 commission | Commission per lot (e.g., $5–$7 round turn) |

Conflict of Interest | Depends on broker execution model | Possible in Market Maker model | Lower, due to ECN routing |

Transparency | High if fee structure clearly disclosed | Moderate to high | High, with visible raw pricing |

Execution Speed | Similar to Standard or ECN equivalent | Fast (broker dependent) | Typically fastest (direct liquidity access) |

Market Access | Same instruments as standard account | Full broker instrument list | Full broker instrument list |

Conclusion

Islamic (Swap-Free) Forex accounts provide Muslim traders with access to global financial markets while eliminating overnight interest charges in compliance with Sharia principles. However, removing swap does not automatically mean lower trading costs.

Brokers may apply alternative pricing models such as administrative fees, wider spreads, or commission adjustments to maintain commercial balance.

A well-structured Islamic account should provide transparent costs, clear holding policies, and strong regulatory oversight. Comparing spreads, commissions, and administrative rules is essential before committing capital to any swap-free trading environment.

For a comprehensive understanding of how we evaluate brokers, please refer to TradingFinder detailed Forex methodology article.